Creative Planning doesn’t operate as a family office but instead provides family office-style advisory services to ultra-high-net-worth families. This article is intended to provide educational information to help you explore the range of family office structures and options available to manage your wealth.

Key Takeaways

- Understand what UHNW wealth management services are and how they differ from standard wealth management models.

- Learn the key components of an integrated UHNW strategy, including investment management, tax optimization, estate planning, philanthropy and family office services.

- See how wealth preservation, global diversification, luxury asset management and alternative investments work together to support long-term growth.

- Explore tax optimization, estate planning and governance approaches tailored to ultra-high-net-worth families.

- Discover how Creative Planning’s planning-led UHNW wealth management services can help align your wealth with your multigenerational goals.

Ultra-high wealth can open doors, but it also introduces layers of complexity that standard wealth management simply isn’t built to handle. When your balance sheet includes operating businesses, significant real estate, private investments and multigenerational goals, you need UHNW wealth management services that coordinate every moving part under one plan.

In this guide, we’ll define UHNW wealth management, walk through the key components of a comprehensive strategy and highlight the advanced tools families use to preserve, grow and transfer substantial wealth.

Introduction to UHNW Wealth Management Services

Ultra-high-net-worth (UHNW) individuals are commonly defined as those with at least $30 million in investable assets, though many firms set that bar even higher. At the same time, many families begin facing “UHNW-level” complexity well before that threshold, particularly in the $5 million-$30 million range that Creative Planning identifies as rising ultra-affluent. At this level, your financial life may span closely held companies, concentrated stock positions, global real estate, alternative investments and complex family dynamics.

At Creative Planning, we recognize that the $10 million mark is a critical inflection point where standard wealth management often reaches its limits. At this level, your financial life requires a more sophisticated family-office-style approach to integrate alternative investments and complex family dynamics into a single, cohesive plan. This is often where families start to consider family office-style support, even if they don’t yet identify as a “traditional” UHNW family.

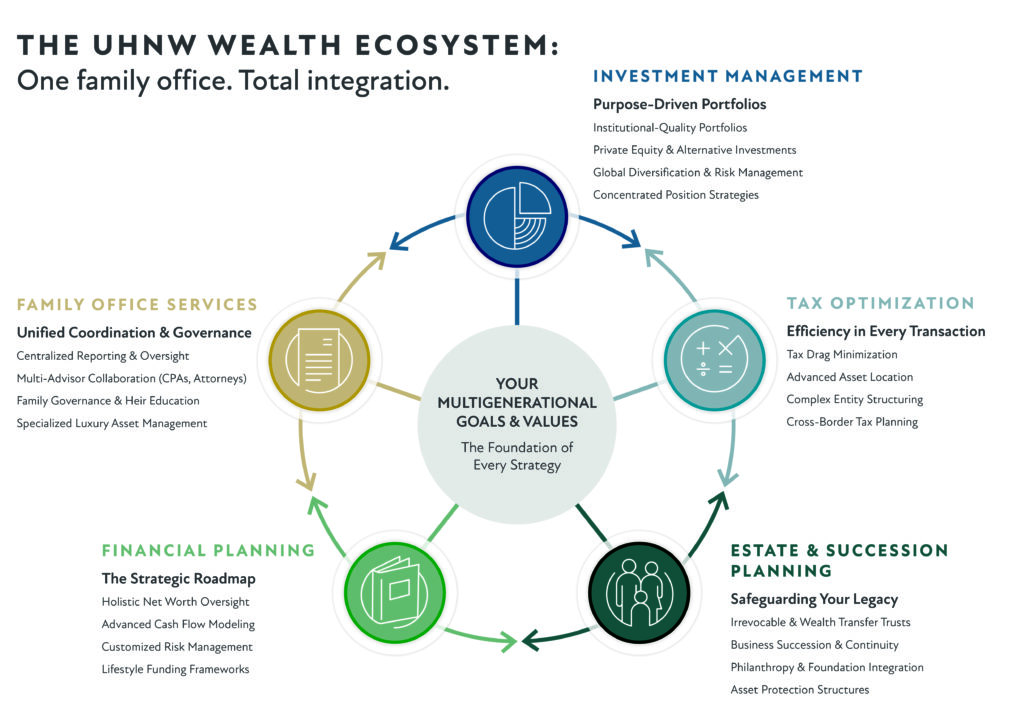

UHNW wealth management services are built specifically for this level of complexity and go far beyond traditional wealth management, focused only on investments and basic planning. An UHNW strategy typically integrates:

- Comprehensive financial planning and wealth preservation strategies

- Institutional-quality investment management and risk management

- Tax optimization for UHNW families, including cross-border planning where relevant

- Estate planning for UHNW individuals and families

- Philanthropy and charitable giving solutions

- Dedicated family office-style advisory services and governance support

Unlike standard advisory relationships, UHNW wealth management brings together your advisors — legal, tax, estate and investment — so that decisions are made in a coordinated way. To see how a planning-led approach looks in practice, explore Creative Planning’s overview of ultra-high-net-worth wealth management.

Key Components of UHNW Wealth Management

While every family’s goals are unique, most UHNW wealth management strategies rely on a common set of components that work together to support the broader plan.

Advanced investment management

UHNW investment management often extends far beyond a traditional portfolio. A comprehensive strategy might include:

- Public stocks and bonds tailored to your risk profile

- Alternative investments, such as private equity, private credit and hedge funds

- Real estate investment strategies across multiple regions

- Luxury asset management for assets like art, aircraft or yachts

- Opportunistic investments that fit within a disciplined framework

While Creative Planning typically doesn’t recommend hedge funds for most clients, these strategies can still be considered for UHNW families when they fit a clearly defined objective, risk budget and overall plan.

These investment decisions are most effective when evaluated alongside your cash flows, tax position, estate plan and long-term legacy goals, not in isolation. If you’d like to see how Creative Planning approaches investing for affluent families more broadly, review our high-net-worth financial planning and wealth management services.

Tax optimization and planning

Effective tax optimization for UHNW families looks at the full picture — current income, realized gains, estates, trusts and entities. It can include:

- Coordinating investment strategy with tax planning (asset location, gain and loss management)

- Designing and funding trusts to manage estate and gift tax exposure

- Structuring entities for operating businesses and real estate holdings

- International tax planning when you or your heirs have global ties

The goal isn’t to let taxes drive every decision but rather to reduce tax drag so that more of your wealth supports your priorities.

Estate planning and succession planning

Estate planning for UHNW families must address both the technical and human sides of wealth transfer. Key elements often include:

- Coordinated wills and revocable trusts

- Irrevocable trust strategies to manage estate and gift tax exposure

- Business succession planning for owners and entrepreneurs

- Provisions for charitable giving, both during life and at death

- Clear governance around who makes decisions and when

Creative Planning’s broader UHNW family planning resources help illustrate how these strategies work together to support long-term legacy goals.

Family office services and governance

Family office services are a hallmark of UHNW planning, whether delivered through a single-family office or multi-family office model. These services typically cover:

- Centralized reporting and oversight of all entities and investments

- Coordination with attorneys, CPAs and other outside professionals

- Family governance structures for decision-making and conflict resolution

- Education for rising generations on stewardship, wealth and responsibility

If you’re weighing whether a multi-family office is right for your situation, our explanation of the multi-family office structure, services and fees provides a helpful framework.

Strategies for Wealth Preservation and Growth

Once you’ve built substantial wealth, the central question often shifts from “How do I grow this?” to “How do I preserve this and still create opportunities?” Effective wealth management strategies focus on both sides of that equation.

Balancing risk and growth

UHNW portfolios are often designed by purpose, such as lifestyle, safety, legacy, opportunity and/or philanthropy. Within that framework, your team can:

- Stress-test the portfolio for different market and economic scenarios

- Manage concentration risk in a business or single security

- Use insurance and legal structures for risk management

- Maintain sufficient liquidity for spending needs and new investment opportunities

This approach helps protect your downside while preserving room for long-term growth.

Diversification and global opportunities

Global investment opportunities can be particularly powerful at the UHNW level, because you can access markets and structures that aren’t always available to smaller investors. A diversified plan may include:

- International equities and fixed income

- Global private equity or private credit

- Real estate across multiple geographies

- Thematic or sector exposures aligned with your outlook

A planning-led firm can help ensure global allocations stay aligned with your risk tolerance, tax picture and estate plan.

Managing luxury and lifestyle assets

Luxury asset management is another specialized element of UHNW wealth management services. For assets like aircraft, yachts, art or collections, you may need to coordinate:

- Acquisition and financing structure

- Ongoing operating, maintenance and insurance costs

- Ownership entities to help manage liability and privacy

- Strategies for eventual sale or transfer to heirs

Handled thoughtfully, these assets can complement — rather than complicate — your broader strategy.

Alternative investments and private equity

Alternative investments and private equity often play a larger role in UHNW portfolios than in typical high-net-worth strategies. When used appropriately, they can provide diversification and access to unique opportunities.

Common options include:

- Private equity and venture capital funds

- Private credit and direct lending

- Hedge funds and other absolute return strategies

- Real assets, such as infrastructure, commodities and specialty real estate

Because alternatives are often illiquid and complex, they require a disciplined approach to due diligence and sizing. A strong process typically includes careful manager selection and ongoing monitoring, clear limits on illiquid exposure relative to your overall portfolio, scenario analysis around capital calls and distributions, and integration with your tax strategy and estate plan.

Tax Optimization Techniques for UHNW Clients

Tax optimization for UHNW families is an ongoing process rather than a one-time project. It typically involves close collaboration among your wealth manager, CPA and estate planning attorney.

Minimizing tax drag on investments

From an investment standpoint, UHNW tax optimization can include:

- Placing tax-inefficient assets in more tax-advantaged accounts where possible

- Managing when and how gains are realized

- Using tax-loss harvesting in volatile markets

- Coordinating charitable strategies with concentrated positions

These tactics are most effective when they’re integrated into your broader UHNW wealth management services, not treated as afterthoughts.

International and multi-jurisdictional planning

For UHNW families with homes, businesses or family members in multiple jurisdictions, international tax planning can be essential. The right strategy may require:

- Understanding residency and domicile implications

- Navigating tax treaties and potential double taxation

- Structuring cross-border ownership for efficiency and asset protection

Sophisticated wealth advisors who specialize in UHNW planning — including firms like Creative Planning — can coordinate this work across your full team.

Estate Planning Essentials for UHNW Individuals

A strong estate plan makes it easier for your family to carry out your wishes during times of transition or uncertainty. For UHNW families, this usually means going beyond the basics.

Key elements of an UHNW estate plan

An effective estate plan for ultra-high-net-worth individuals often includes:

- Wills and revocable trusts that reflect your current wishes

- Carefully designed irrevocable trusts to manage estate and gift tax exposure

- Business succession planning and governance, if you’re an owner or founder

- Charitable vehicles, such as donor-advised funds or foundations

- Coordinated beneficiary designations and titling across accounts

Addressing common challenges in UHNW estate planning often requires both technical strategy and careful communication.

Addressing common challenges

Common challenges in UHNW estate planning include:

- Balancing “equal” and “fair” among children and other heirs

- Planning for blended families and multiple generations

- Managing privacy concerns around public filings or philanthropic activity

- Preparing heirs for both the responsibility and complexity of wealth

Regular reviews — especially after major life events or law changes — help keep your estate plan aligned with your values and goals.

Philanthropy and Charitable Giving Options

For many ultra-high-net-worth individuals, philanthropy is one of the most meaningful aspects of their financial life. When integrated thoughtfully, charitable giving can support causes you care about, reinforce family values and complement your tax and estate planning.

Choosing your giving vehicles

UHNW philanthropy options include:

- Direct gifts to organizations

- Donor-advised funds for flexible, ongoing giving

- Private foundations for families that want more control and visibility

- Charitable trusts that can provide income to you or your heirs while benefiting charities

Each vehicle has different implications for control, privacy and tax treatment, so it’s important to align your choices with both your goals and your broader strategy.

Creative Planning’s resources on philanthropy and charitable giving, including insights on tax-smart year‑end giving, offer practical examples of how UHNW families integrate giving into their overall plan.

Integrating philanthropy into your wealth plan

When philanthropy is part of your UHNW wealth management services, it can help:

- Instill shared values and a sense of purpose across generations

- Provide a structured venue for family collaboration and education

- Create potential tax efficiencies when coordinated with other planning tools

Many families treat philanthropy as both a legacy and a training ground for younger family members to learn decision-making, due diligence and stewardship.

Bringing It All Together

UHNW wealth management services are about much more than managing a portfolio. They’re about bringing investment management, tax optimization, estate planning, philanthropy and family office-style advisory services into one cohesive plan that reflects what you want your wealth to accomplish.

Creative Planning provides integrated UHNW wealth management services, including family office-style advisory services, sophisticated investment and tax strategies, and family governance support for ultra-high-net-worth families. Our planning-led approach is designed to help you grow, protect and transfer wealth across generations while freeing you to focus on what matters most.

If you’d like to see how this type of strategy could work for your situation, consider connecting with Creative Planning to discuss your goals, wealth complexity and family dynamics with a team experienced in UHNW and family office planning.